Over the past decade, local investors increasingly turned their attention to offshore investments to diversify portfolios and safeguard wealth across the global financial landscape. It is important for investors to know what to look out for when investing offshore, when selecting the type of investment vehicle to use and the tax implications of redeeming investments.

| Over the past decade, local investors increasingly turned their attention to offshore investments to diversify portfolios and safeguard wealth across the global financial landscape. It is important for investors to know what to look out for when investing offshore, when selecting the type of investment vehicle to use and the tax implications of redeeming investments. | DOWNLOAD PDF |

South Africa follows a residence-based tax system. This mean that if you are a South African tax resident you must declare and pay tax on worldwide income. It is imperative for investors to understand how these offshore (discretionary) investments are taxed in South Africa since not all offshore investments are the same and the tax implications can vary between them.

In this article, we briefly highlight the three most common types/vehicles of discretionary offshore investments for individuals and explain how each is treated for tax on redemption of the investment.

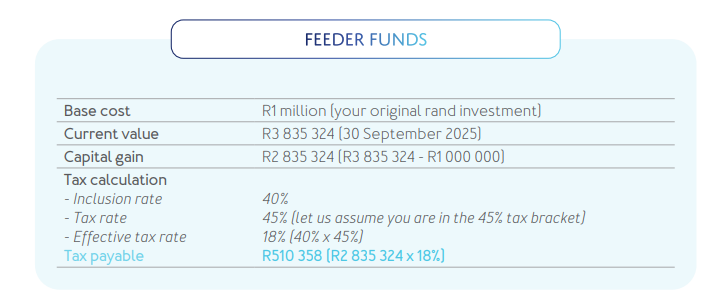

Envisage that it is 2015. You invested R1 million offshore when the rand was at R14 to the US dollar, giving you an investment of $71 429. Your investment was a passive one, tracking the MSCI AC World Index. Fast forward ten years to September 2025. The rand has weakened to R17.29, the MSCI ACWI has achieved an annualised return of 12% and your investment has grown to $221 805, or R3 835 324 in rand terms. You have done well over the ten years thanks to a combination of market growth and currency depreciation.

But then comes the question that catches many investors unawares, “what about tax when you dispose of your investment?”

Feeder funds offer South African investors a convenient way to access offshore markets without having to move money abroad themselves. You invest in rands, and the asset manager takes care of converting your investment into foreign currency and allocating it to a larger offshore fund, typically through an asset swap process. This means you gain exposure to offshore assets, while staying within the South African financial system.

Because your base cost is in rands, the weakening of the rand works against you – inflating both your capital gain and your tax bill.

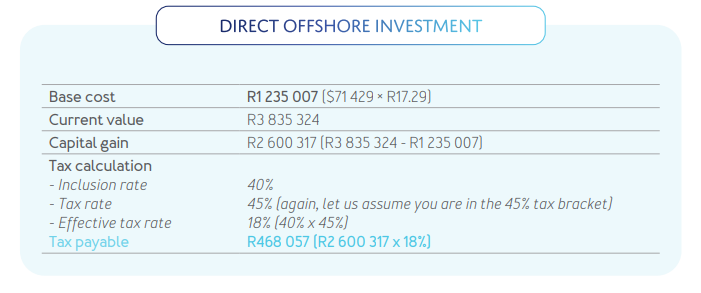

Direct offshore investing means putting your money straight into a foreign currency, such as the US dollar. Unlike feeder funds, investors bypass the rand-based structure and asset swap process. This approach provides full exposure to offshore markets and allows the base cost of your investment to eliminate any currency movements.

Because your base cost is converted at the current exchange rate, the rand’s depreciation assists you — reducing your capital gain and saving more than R40 000 in tax when compared to the feeder fund.

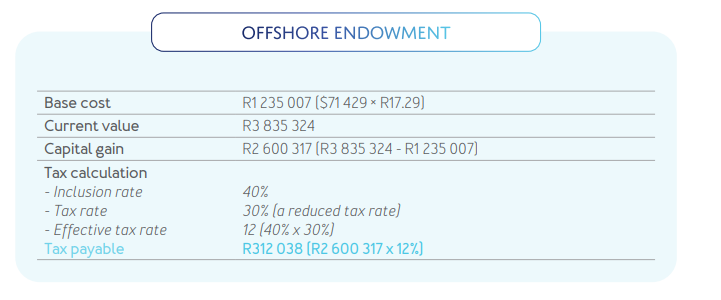

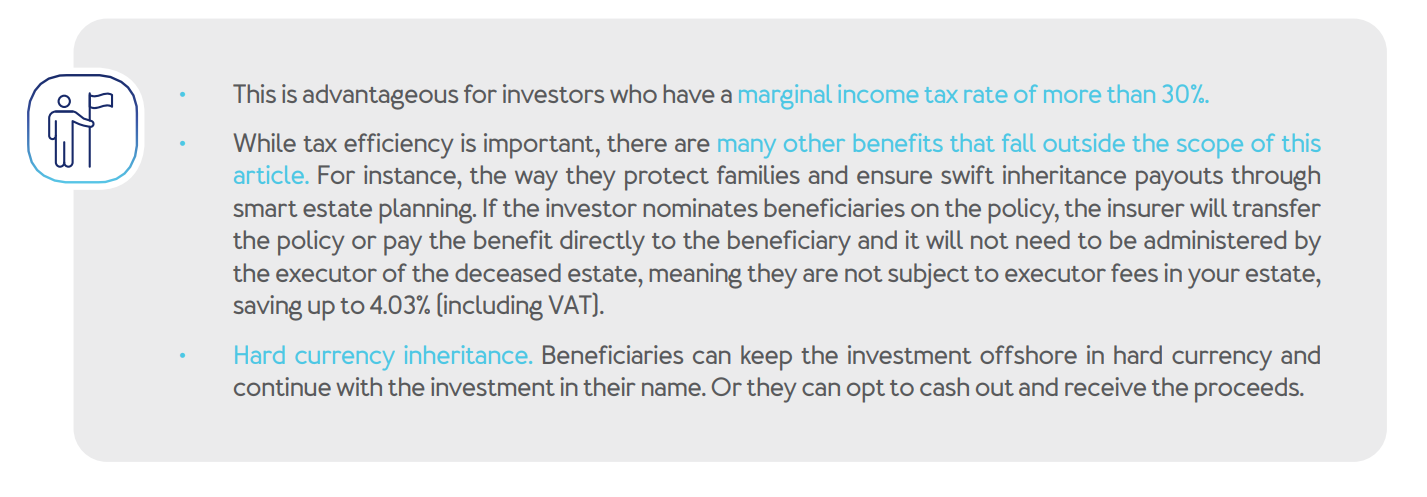

With an offshore endowment, you again invest directly offshore in hard currency, but through an offshore tax wrapper. This is a specialised investment structure issued by a South African insurer that allows you to invest in a hard currency like the US dollar. You can also use your first R1 million without tax clearance. The main difference is that your tax rate is lower.

For individual investors, the income from the investment will be taxed at a rate of 30%. With a capital gains tax inclusion rate of 40%, the effective rate of capital gains tax will only be 12% for high income earners that are in the 45% tax bracket.

The decision as to which investment vehicle/fund to consider when investing offshore is not a simple one. A significant issue to consider when selecting a fund/vehicle is the impact of CGT. The same investment, with the same growth, can result in different tax outcomes depending on how it has been structured. It is therefore important for investors to familiarise themselves with CGT calculations when investing offshore.

Apart from the CGT differences, remember that each of these vehicles has distinct benefits that include the CGT treatment. Hence, investors need to ensure they add CGT implications to the list when making a full comparison across the respective vehicles.