The first quarter of the year was overshadowed by the war in the Middle East.

MIDDLE EAST CONFLICT RATTLES WORLD MARKETSA month into the war, investors continue to be whipsawed by a barrage of headlines as tensions and attacks between the US, Israel and Iran escalate — a period where the world’s financial markets have been tossed around at the mercy of geopolitics. Oil prices have seen their second-biggest quarterly rise of the century, Europe’s gas prices have almost doubled and global interest rates are suddenly pointing up, rather than down.The new year has not only been about Iran and the oil price. Things got off to a wild start, with the US capture of Venezuela’s President Nicolas Maduro, followed by Donald Trump’s demands to take control of Greenland. All of this happened in a quick space of time despite ongoing uncertainty around US trade policies — with the US Supreme Court ruling to overturn the Trump administration’s sweeping global tariffs — and the impact AI development may have on the business models of global software companies. Oil spikedThe past century has shown that even the world’s largest and most modern militaries can be forced to eat humble pie when attacking enemies willing to defend their territory despite overwhelming odds. Tehran has taken control of the Strait of Hormuz using far less sophisticated weaponry than the US, effectively ‘choking’ energy supplies and commercial shipping through the vital waterway, to drag the US into a potential ‘drawn out’ war. This is not good for energy prices, inflation and ultimately global growth.The war in Iran started on 28 February. The oil price moved sharply higher on fears of supply disruptions, within a whisker of $120 a barrel at one point — at the time of writing the oil price was at $105 a barrel — up 70% YTD. The near-total closure of Hormuz has resulted in millions of barrels of lost daily oil output, while supercharging product prices from diesel to jet fuel. | DOWNLOAD PDF |

Iran is a sizeable oil producer, the fourth largest within OPEC, accounting for roughly 4% of global oil supplies, with about 80% of its exports going to China. Iran also sits in a strategically important position since it is able to control access to the Strait of Hormuz, a critical bottleneck through which approximately 20% of the world’s oil supply passes, as well as a meaningful share of global liquefied natural gas (LNG) production. Where the oil price goes from here is anyone’s guess. The International Energy Agency said the closure of the Strait of Hormuz has triggered the largest disruption to global oil markets in history, with supply expected to fall by about 8 million barrels per day in March, or around 8%. The agency’s member countries responded by agreeing to release a record 400 million barrels from strategic stockpiles in an attempt to stabilise oil prices and compensate for the loss of Middle East output.

| Economists and businesses increasingly believe the disruption to world oil supply will filter through to inflation worldwide — a drawn-out energy crisis will sooner or later hit every corner of the global economy.

The combination of higher energy costs (inflation) and slower global economic growth creates a ‘cost-push’ stagflationary scenario. Investors are now seriously considering a stagflationary shock. The risk of a 1970s scenario is emerging, where disruption to global energy supplies sent inflation surging and slowed global growth. The inflationary pressure from energy costs has forced central banks to pause interest rate cuts and even consider raising them, despite slowing economic growth. The US Fed, European Central Bank and the Bank of England all held rates in March as policymakers grappled with the uncertain outlook. The Bank of Japan postponed a possible rate hike. Markets sharply downGlobal financial markets have entered a pronounced ‘risk-off’ mode, resulting in increased volatility, capital outflows from emerging markets and a rush towards safe-haven assets. The US dollar has become the safe haven of choice during the turmoil, putting most other currencies under pressure, and has gained 2% against a basket of currencies. |  |

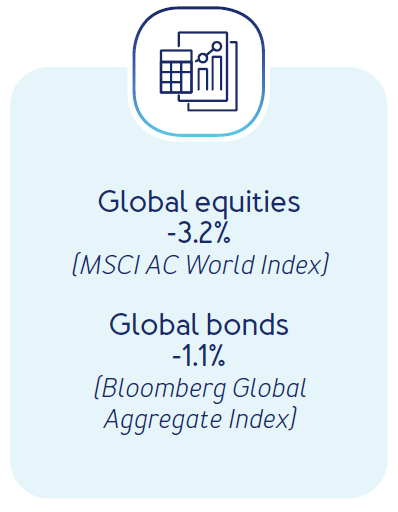

The MSCI AC World Equity Index ($) was down 3.2% in Q1. Global equities outside the US extended their early-year rally until late February, when a sharp pullback followed, underscoring how quickly geopolitical shocks can upend market momentum. Regionally, it can be argued that Asia and Europe are particularly exposed to the conflict given their reliance on imported oil that moves through Middle Eastern shipping lanes. The MSCI Emerging Market Index ($) was flat in Q1 (-0.1%), after dropping 10% in March. Government bond yields rose, as central banks are seen as more likely to raise interest rates to head off a potential inflationary shock from higher energy costs. The Bloomberg Global Aggregate Global Bond Index fell 1% in dollar terms in Q1.

The US Fed decided to leave interest rates unchanged at a range of 3.50% to 3.75%. A lack of progress in bringing an end to the Middle East conflict is beginning to sap consumer and business confidence. The University of Michigan’s index of US consumer sentiment fell more than expected in March, touching a three-month low. Economic growth is under pressure due to a combination of high tariffs raising costs, slowing labor markets, and massive federal debt interest.

The US economy is projected to grow by approximately 1.8% to 2.0% in 2026, reflecting a moderate, resilient pace after it expanded by 2.1% in 2025. While many economists still view a hike as unlikely, the market has completely shifted away from anticipating rate cuts, expecting higher rates to persist in combating inflation.

Wall Street’s main indices all fell sharply in Q1 on concerns around escalation in the US-Israeli war against Iran and ongoing capital spending by tech companies. Collectively, the tech giants are expected to spend at least $630 billion this year on AI. The S&P 500 Index and Nasdaq Composite fell by 4.3% and 6.9% respectively in Q1.

Investors have retreated from the big tech names that carried the market in recent years, putting downward pressure on shares. The Software (Industry) Index was down 24% in dollar terms in Q1. Investors are worried that artificial intelligence (AI) is about to upend the business model of selling enterprise software — if AI agents can code, companies can just build their own software suites and cut out the companies they once bought them from. If AI tools become good enough, fast enough, soon enough, to replace software, these well-known software companies might be vulnerable. The jury is out but according to Anthropic their new Claude agent tool could replace dozens of software tools.

Uncertainty about the duration of the conflict also drove US bond yields higher as investors reassessed the upside risk to inflation and the outlook for Federal Reserve monetary policy. Markets have abruptly shifted from pricing in rate cuts to factoring in potential interest rate hikes in 2026. The 10-year US Treasury yield, which sets the tone for borrowing costs around the world, rose 12 basis point to 4.3%. The Federal Reserve is now expected to keep rates on hold this year, compared with more than 50 basis points worth of easing priced in prior to the start of the war. The surge in bond yields has added to concerns over other market segments being at risk of overheating, such as the private credit market.

‘Private credit’ does not have one set definition. Rather, it is an umbrella term referring to a handful of debt investment strategies. It is ‘private’ because unlike traded forms of debt where banks are typically involved in arranging the transactions, the details are often invisible to anyone not connected to the deals.

| Many worries are hitting the $1.8 trillion private credit market after it enjoyed tremendous growth over the past decade when policy rates were near-zero and investors sought alternatives to low-yielding products. Private credit delivered, offering a differentiated source of income, the potential to outperform public markets, and healthy yields with lower volatility. Recently, however, the narrative

has shifted. Some market participants worry that private credit poses systemic risk to financial markets, setting off a scramble by some investors to withdraw money from industry’s giants.

In Q1, assets managed by firms such as Apollo Global Management Inc., BlackRock Inc. and Ares Management Corp. faced unprecedented requests for redemptions and, in many cases, have exercised their right to block investors from getting all their money out. Most of the funds facing redemption requests are in a subset of private credit known as direct lending, where investment firms lend money to riskier, typically privately owned companies. Investors are attracted to these deals because they offer high yields, in exchange for taking on more risk. |  |

European markets posted their steepest monthly decline in nearly four years, with the STOXX 600 Index falling 8% in March, ending an eight-month rally. The index slipped 1.5% for Q1 2026, marking its first quarterly decline in five quarters amid heightened Middle East tensions. Inflation in the eurozone edged up to 2.5% in March, reinforcing concerns around persistent price pressures — as energy costs rose because of the war — and pushed headline inflation back above the European Central Bank’s 2% target.

The Chinese economy has demonstrated remarkable resilience, despite domestic challenges. Growth is nevertheless expected to be lower at 4.5% in 2026, compared to 5% last year. This may now be impacted by the war in the Middle East. The CSI 300 Equity Index lost 3% in Q1. Tech shares fell, tracking their US peers in a mix of profit-taking and concerns over the impact of AI. Beyond tech, shares continued to be bogged down by uncertainty over the war.

Goldman Sachs strategists believe the Chinese economy is better positioned than other nations to withstand the historic oil shock from the ongoing war in Iran. Crude oil and liquified natural gas made up 28% of China’s primary energy consumption in 2024, the lowest in the world. Further, alternative and renewable energy accounted for 40% of China’s electricity generation over the same period. Another factor cushioning the Chinese economy is its substantial oil reserves. If crude imports were to come to a complete halt, China has enough oil in strategic and commercial reserves to meet the nation’s supply needs for 110 days.

Japan continued to grapple with elevated energy costs driven by the Iran war. More than 90% of Japan’s oil is reliant on Middle Eastern imports, largely passing through the now-blocked Strait of Hormuz. Japan is considering releasing its strategic petroleum reserves, which hold over 200 days of supply, to manage the disruption. The Nikkei 225 Index was marginally positive, up 1.4% in dollar terms for Q1, despite dropping 13% in March.

The South African Reserve Bank (SARB) kept the policy rate unchanged at 6.75% at its March meeting, as expected amid the war in the Middle East. Overall, SA’s headline inflation rate remains well contained — headline CPI fell to 3.0% y/y in February from 3.5% in January, breaching the SARB’s revised inflation target for the first time.

However, the surge in SA’s fuel price is going to undermine the recent success in bringing inflation well under control. This does not mean that inflation is going to remain significantly more elevated on a sustained basis, but it does highlight the importance of ending the Middle East conflict as soon as possible and at the same time getting the oil price substantially lower. It is also important to recognise that over the past 12 months SA’s inflation outcome has benefitted from a convergence of numerous positive factors that are not all likely to persist over the next 12 months — for example the recent currency weakness that has accompanied the Middle East conflict. Consequently, SA monetary and fiscal policy still has a lot of work to do to ensure that the new inflation target of 3% is embedded and used as the key reference for future price increase.

| Geopolitical risks in the Middle East weighed on risk sentiment in emerging markets. The rand weakened 2.3% against the US dollar and the JSE All Share (Total Return) Index fell 0.6% in Q1. The local bourse dropped 10% in March alone, as investors shifted towards safe-haven assets amid intensifying geopolitical uncertainty. The big losers in Q1 on the JSE were big industrial index shares, such as Richemont and Naspers/Prosus. Overall, the industrial sector lost 8.7%, financials were flat (-0.2%) and resources positive (8%), despite being down 15% in March. Sasol bucked the trend, with the share price up a staggering 112% in Q1, on the back of the steep increase in the oil price. |  |

| Gold is usually considered a haven asset, offering investors safety during times of volatility. So why did the gold price fall by 12% in March — although still up 8% YTD. The precious metal has become the latest victim of rising inflation expectations and dimming hopes of global interest-rate cuts. A stronger dollar and rising bond yields make non-yielding gold less attractive. Increased inflation, partially driven by oil shocks, caused investors to shift from gold into safer dollar-based assets, alongside profit-taking after previous record highs. Gold tends to thrive when rates are lower — higher demand for non-yielding assets — and the opportunity cost of holding the metal is low. But when rates are higher, investors tend to ditch the metal in favour of other assets that can offer a higher return. |  |

| Foreign investors dumped SA government bonds in March due to the geopolitical uncertainty and the reduced likelihood of any further rate cuts. This was a sharp turnaround from the first two months of the year, when foreign investors were net buyers of debt, according to National Treasury data. The reversal ended a period of heavy foreign buying, as investors cashed in on significant profits from the recent bond rally that drove South African yields to decade-lows in February.

In another sign of nervousness, the cost of insuring SA’s debt against default over five years via credit-default swaps, climbed to a five-month high in Q1. Since the war started, the Government 10-year yield has jumped more than 90 basis points, among the highest in emerging markets. The risk-off trade resulted in the JSE All Bond Index dropping 3.4% in Q1. |  |

Money market assets preserved capital and gained a respectable 1.66% in Q1, up 7.2% over 12 months.